Bondrewd

Veteran

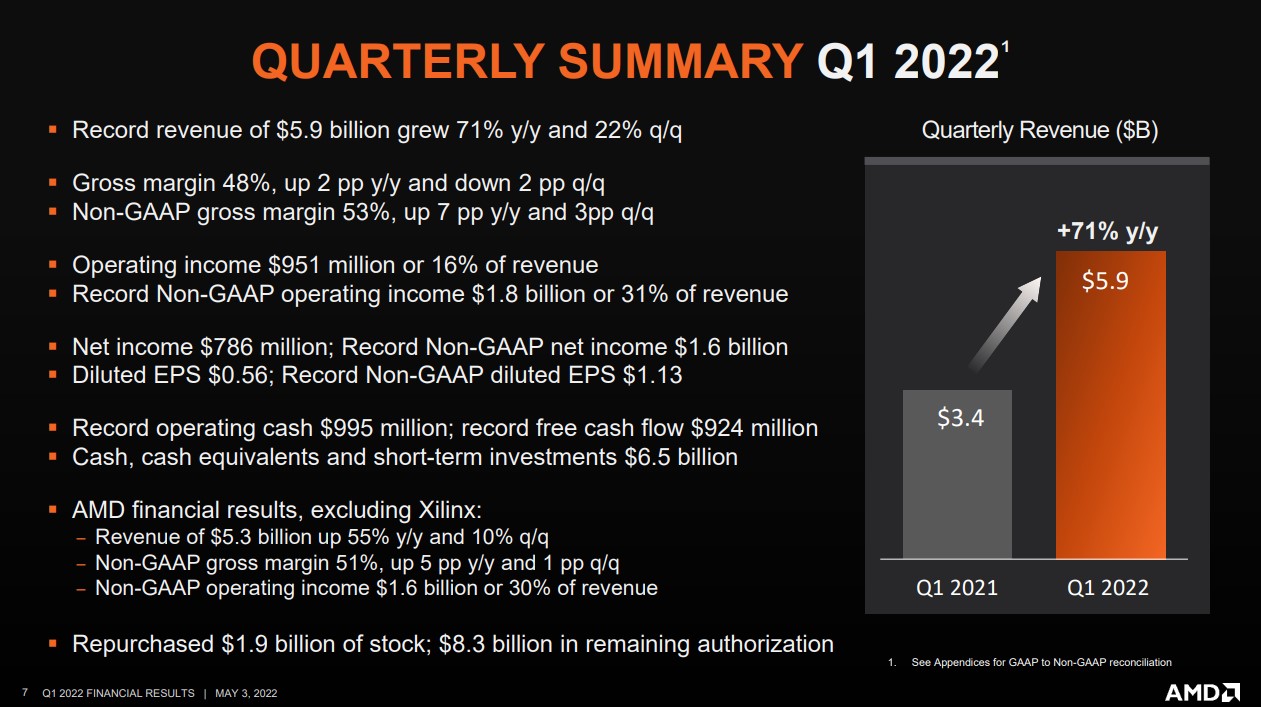

RIPperoni go my moneys this Q

wow, all the gap looks to be in client,

RIPperoni go my moneys this Q

Still the effects of the pandamic/ETH etc.

AMD's acquisition of field programmable gate array (FPGA) firm Xilinx boosted its Embedded revenue segment by a whopping 1,549% during this quarter and the previous one, as it enabled the firm to maintain its revenues at a time when consumers are struggling with new computing purchases as inflation bites into their purchasing power

Nope, Client is CPU+chipset (+APU but I count it as just CPU these days, especially now that all AM5 CPUs have GPU). GPUs fall under Gaming together with semicustoms. Also it's not 1549 compared to previous quarter, it's compared to last year. Last quarter already had Xilinx in it, last year didn't.Following NVIDIA, AMD downsized their Q3 revenue, from 6.7B to 5.6B (a drop of 1.1B), citing "poor macroeconomic conditions and a supply chain correction", The bulk of the revenue drop is courtesy of AMD's Client segment (CPUs + GPUs), AMD's acquisition of field programmable gate array (FPGA) firm Xilinx boosted its Embedded revenue segment by a whopping 1,549% during this quarter and the previous one.

AMD Hit With Weak PC Demand As Desktop, Notebook Sales Tank By 40%

AMD has become the latest chip company to be hit with a worsening environment as its desktop sales drop by 40%.wccftech.com

The Data Center segment primarily includes server microprocessors, GPUs, data processing units (DPUs), Field Programmable Gate Arrays (FPGAs) and adaptive SoC products for data centers. The Client segment primarily includes microprocessors, accelerated processing units (APUs) that integrate microprocessors and graphics, and chipsets for desktop and notebook personal computers. The Gaming segment primarily includes discrete graphics processing units (GPUs), semi-custom System-on-Chip (SoC) products and development services. The Embedded segment primarily includes embedded microprocessors, GPUs, FPGAs, adaptive SoC products, and Adaptive Compute Acceleration Platform (ACAP) products. From time to time, the Company may also sell or license portions of its IP portfolio. All Other category primarily includes certain expenses and credits that are not allocated to any of the operating segments. Also included in this category are acquisition-related intangible asset amortization expense, stock-based compensation expense, acquisition-related costs and licensing gain.

Just CPUs.The bulk of the revenue drop is courtesy of AMD's Client segment (CPUs + GPUs).

Which is what I said: this quarter and the previous quarter. In 2021 Xilinx wasn't around, so they added nothing to AMD. But in 2022, Xilinix added 550M (partial revenue) in Q1 2022, added ~1100M (full revenue) in Q2, and ~1300M (expected full revenue) in Q3.it's not 1549 compared to previous quarter, it's compared to last year. Last quarter already had Xilinx in it, last year didn't.

I am getting tired of AMD shuffling their dGPUs revenue around like it's a marionette.Nope, Client is CPU+chipset

www.servethehome.com

www.servethehome.com

ir.amd.com

ir.amd.com

It's more tidy this way I admit. But it's still really hard to track down their consumer dGPUs alone, as AMD insists on always bundling them together with "something", either with console SoCs, or with Ryzen CPUs, then back again with console SoCs.

Wild that Intel somehow has 4% share of the discrete market.In Q3, AMD dGPUs share dropped to an all time low of 8%, NVIDIA stands at 88%.

Q3 2022 Discrete GPU Market Share Report: NVIDIA Gains 88% Market Share Hold, AMD Now at 8% Followed By Intel at 4%

Jon Peddie Research (JPR) has published the full GPU market share report for Q3 2022 that cover AMD, Intel & NVIDIA GPUs.

AIBs.Those numbers are shipped by IHVs, aren't they?

I don't know what you mean here when you then talk about numbers shipped by IHVs.AIBs.

Ouch, the strongest GPU shipment quarter saw a massive drop in overall GPU shipments. Inflation and fears of a recession hitting hard combined with the crash in crypto-currencies.

-25.1 year over year for all GPUs and -10.3% quarter to quarter. It's extremely rare for shipments to drop going from Q2 to Q3 since Q3 is generally the highest selling quarter for GPUs.

Desktop discrete was particularly bad, -30% quarter to quarter (10 million Q2 down to 7 million Q3) and about 46 million year to year (13 million Q3 2021 down to 7 million Q3 2022).

Overall desktop GPU shipments managed to increase due to increase in integrated desktop GPU shipments which was helped by all new AMD Ryzen consumer CPUs now including integrated GPUs.

Ouch, it's a slaughter.

Regards,

SB

:max_bytes(150000):strip_icc()/GettyImages-1162946945-58d990392cef43d993dd3fc6c682d592.jpg)

Jon Peddie collects the numbers from AIBs.I don't know what you mean here when you then talk about numbers shipped by IHVs.

Those aren't the only customers. So that, at best, is only the partial truth.Jon Peddie collects the numbers from AIBs.

Yeah, Data Center GPUs from AMD, NVIDIA or Intel are not accounted for here, same for GPUs for the Edge/Embedded, or Professional Visualization or other exotic use cases (like GPU RAID) .. etc.Those aren't the only customers. So that, at best, is only the partial truth.