I'm willing to bet a lot of money that the majority of that 2.9M is MCP61 for the ultra-low-end desktop market. It does support AM2+ and combined with something like the 117mm² 45nm dual-core Regor chip, it's going to be a lot lot cheaper than Llano, and have much faster CPU performance than Zacate.

So there's still a niche for NVIDIA to be selling AMD IGPs (believe it or not). It's certainly going to go down over time and eventually disappear but I'd expect that to take much longer than 1 or 2 quarters.

There was supposed to be a dual-core ASIC for Llano, with 160SPs, I believe. I don't know if it's actually available yet, but if it is, I'd expect it to be around 130mm², so not that much more expensive.

Still, Jon Peddie seems to agree that most of NVIDIA's remaining IGP market is actually for AMD CPUs. I'm not sure how long it will take for AMD to phase AM2+ out, but once they do, that market is gone.

With Trinity coming up, along with the Brazos refresh, I don't see much point in keeping AM2+ around, unless they can't meet demand with 40/32nm chips alone. We'll see, but I'd be really surprised if the AM2+ market still amounts to anything substantial in a year.

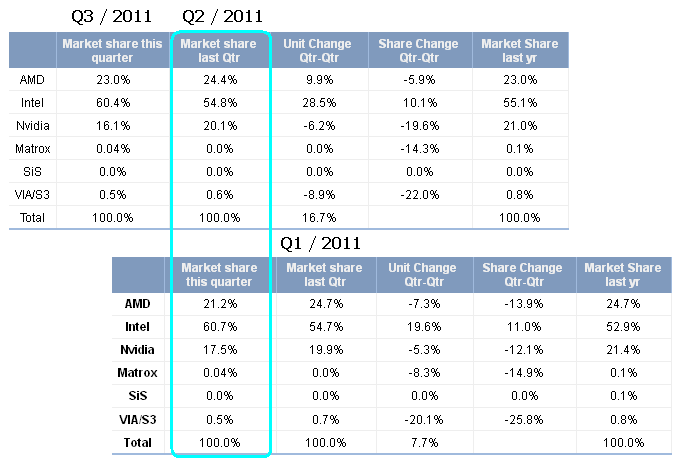

The total share is completely irrelevant for game developers that also target high-end GPUs rather than just the low-end.

Wake me up when NVIDIA has less than 30% discrete desktop share. AMD has been unable to make that happen even in the RV770 era where they had an extremely impressive die size/cost advantage, and NVIDIA has proven they are ready to fight for market share by cutting their margins drastically if that's their only choice. On the other hand, AMD could certainly make a lot of money if they deliver on their 28nm generation.

It wasn't so long ago that integrated GPUs such as Intel's GMA were completely irrelevant for most game developers. They were just too slow for actually playing anything on them, and in fact, many games didn't even

work on them, let alone play smoothly.

I think it's fair to say that this is no longer the case, and that future APUs (from both Intel and AMD) will make it even less true. At some point, developers will start considering APUs as the primary target for (at least mainstream) games and when that happens, they'll have to choose where to spend the largest amount of effort. Intel will be the biggest player, but with relatively slow graphics, while AMD will come second but with faster integrated GPUs, and much faster discrete GPUs based on the same (or a very similar) architecture. How much time will be left to optimize for NVIDIA?

I don't know if this will become reality in 2012, 2013 or even later, but eventually it seems unavoidable.

")